The Central Board of Direct Taxes (CBDT) has notified amendments in the annual salary Tax Deducted at Source (TDS) certificate issued to employees in Form No.16. Part B of Form 16 which provides details of salary paid and other income has been modified asking for more details about the allowances exempt under section 10 and deductions allowed under Chapter VI-A of the Income Tax Act.

Exemptions under section 10:

In the present format of Part B of Form 16, an employer has the option to mention the nature of the allowances exempt under section 10 with the respective amounts. In the absence of a mandatory disclosure requirement, various employers issued Form 16 in different formats. Some employers provided complete disclosure, others aggregated the allowances and disclosed the net amount exempt under section 10.

In new Form 16 notified now, employers have to furnish the amount of allowance against the ear-marked fields. Specific fields are notified for allowances mentioned below:

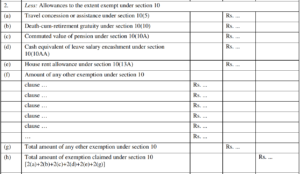

- Leave travel concession exempt under section 10(5)

- Death cum retirement gratuity exempt under section 10(10)

- Commuted value of pension under section 10(10A)

- Leave encashment under section 10(10AA)

- House rent allowance under section 10(13A)

The amount of any other exemption under section 10 has to be mentioned quoting the relevant clause. A snapshot of the details of exemptions is provided below:

Deductions under Chapter VI-A:

Similar to the disclosures for exempt allowances above, employers had the option to present the details of deductions under section 80C to section 80U of the Income Tax Act.

In Form 16 now notified, employers have to furnish the amount of deduction against the ear-marked fields. Specific fields are notified for deductions mentioned below:

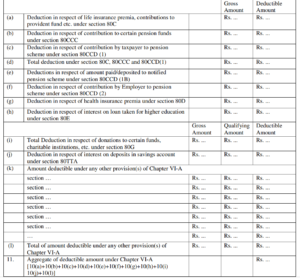

- Deduction for life insurance premium paid, contribution to PPF etc., under section 80C

- Deduction for contributions to pension funds under section 80CCC

- Deduction for employee’s contribution to a pension scheme under section 80CCD(1)

- Deduction for taxpayer’s self contribution to a notified pension scheme under section 80CCD(1B)

- Deduction for employer’s contribution to a pension scheme under section 80CCD(2)

- Deduction for health insurance premium paid under section 80D

- Deduction for interest paid on loan acquired for higher education under section 80E

- Deduction for donations made under section 80G

- Deduction for interest income on savings account under section 80TTA

The amounts entitled for deduction under any other section of Chapter VI-A have to mentioned quoting the respective section.

A snapshot of the details of deductions is provided below:

Other changes:

With reference to any other income reported by an employee, specific fields have been introduced as below:

- Income (or admissible loss) from house property reported by employee offered for TDS

- Income under the head Other Sources offered for TDS

- A field has been introduced for reporting the total amount of salary received from other employers

- A field has been introduced for standard deduction allowed under section 16 of the Income Tax Act.

The new Form 16 is made effective from 12 May 2019. Thus, most employers issuing Form 16 for the financial year 2018-19 will have to issue in the new format. The changes mentioned above to Form 16 will ensure that employers follow a uniform format for reporting of salary with the tax exemptions and deductions thereon.

Also, the amendment is in line with changes introduced in the income tax returns notified for AY 2019-20. This would facilitate employees in the filing of their tax returns for AY 2019-20.

In addition to the above, the move would facilitate the Income Tax Department to cross verify income reported by an employee with the TDS certificate issued by the employer.

I am a Chartered Accountant by profession. I specialise in personal taxes and corporate income tax matters. I am an avid reader and track developments in financial markets, economy and other market developments.